Risk Management, Strike and Structure Selection

... how do we decide on our trade setups?

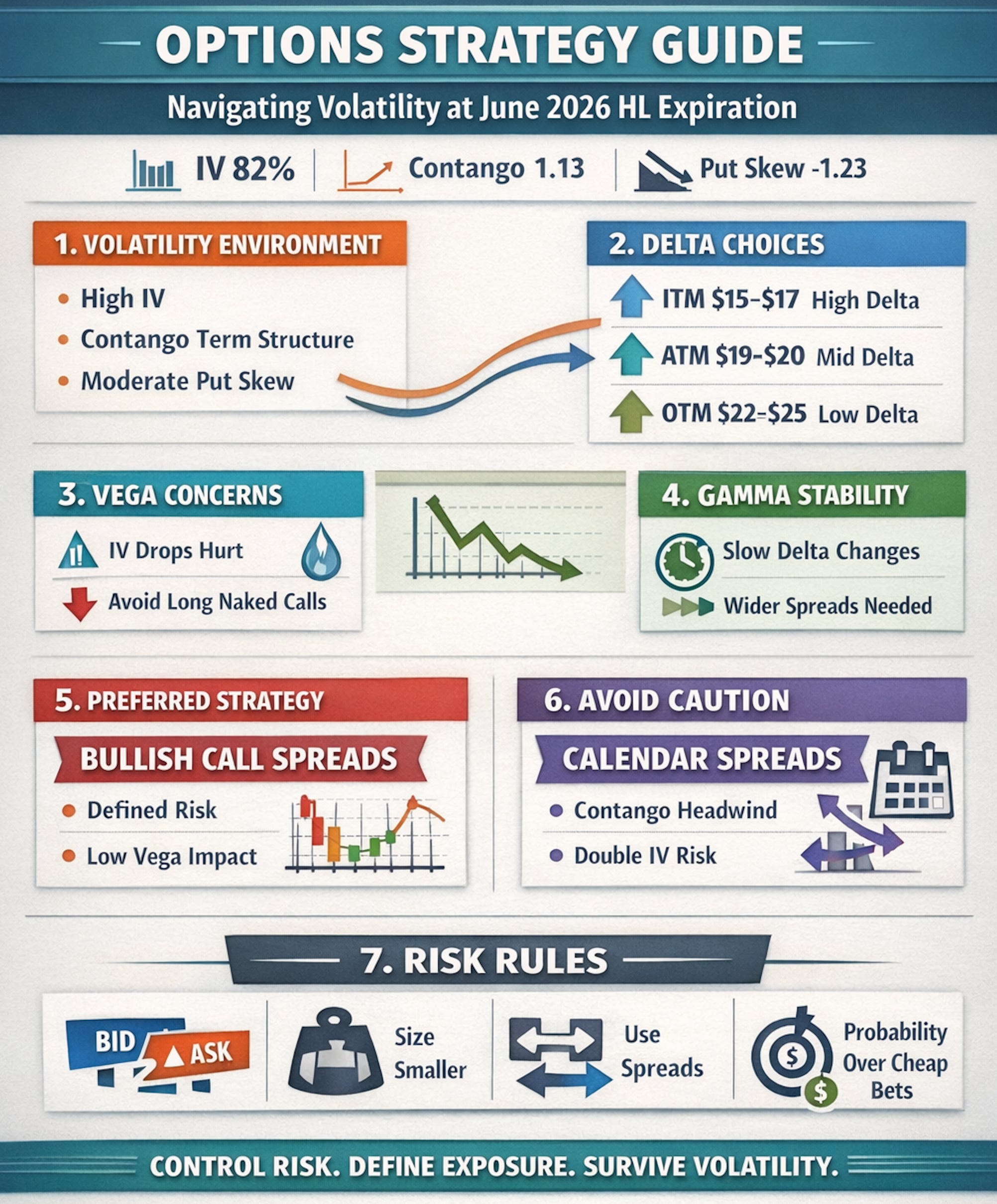

Some of you asked for more clarity around risk management, strike selection, and why we choose certain option structures over others—especially in volatile names. This note is meant to be a clean, practical walkthrough using Hecla Mining Co. - HL (June 2026 options) as a real example.

The goal here is not to predict price. It’s to show how we control the things we can control: risk, exposure, probability, and structure.

1. Start With the Environment — Not the Trade

Before picking strikes or structures, we first define the volatility regime.

HL snapshot (June 2026, ~168 DTE):

Stock: $18.89

6-month IV: ~82%

Ex-earnings IV: ~80%

Term structure: Contango (1.13)

Skew: Moderate put skew (slope ≈ -1.23)

What this tells us:

Volatility is already very high.

Longer-dated options are priced higher than front-month options.

Downside protection (puts) is more expensive than upside calls.

This immediately frames our decision-making:

Long naked options = high vega risk

Calendars = structural headwind

Spreads = preferred tool

Environment first. Trade ideas second.

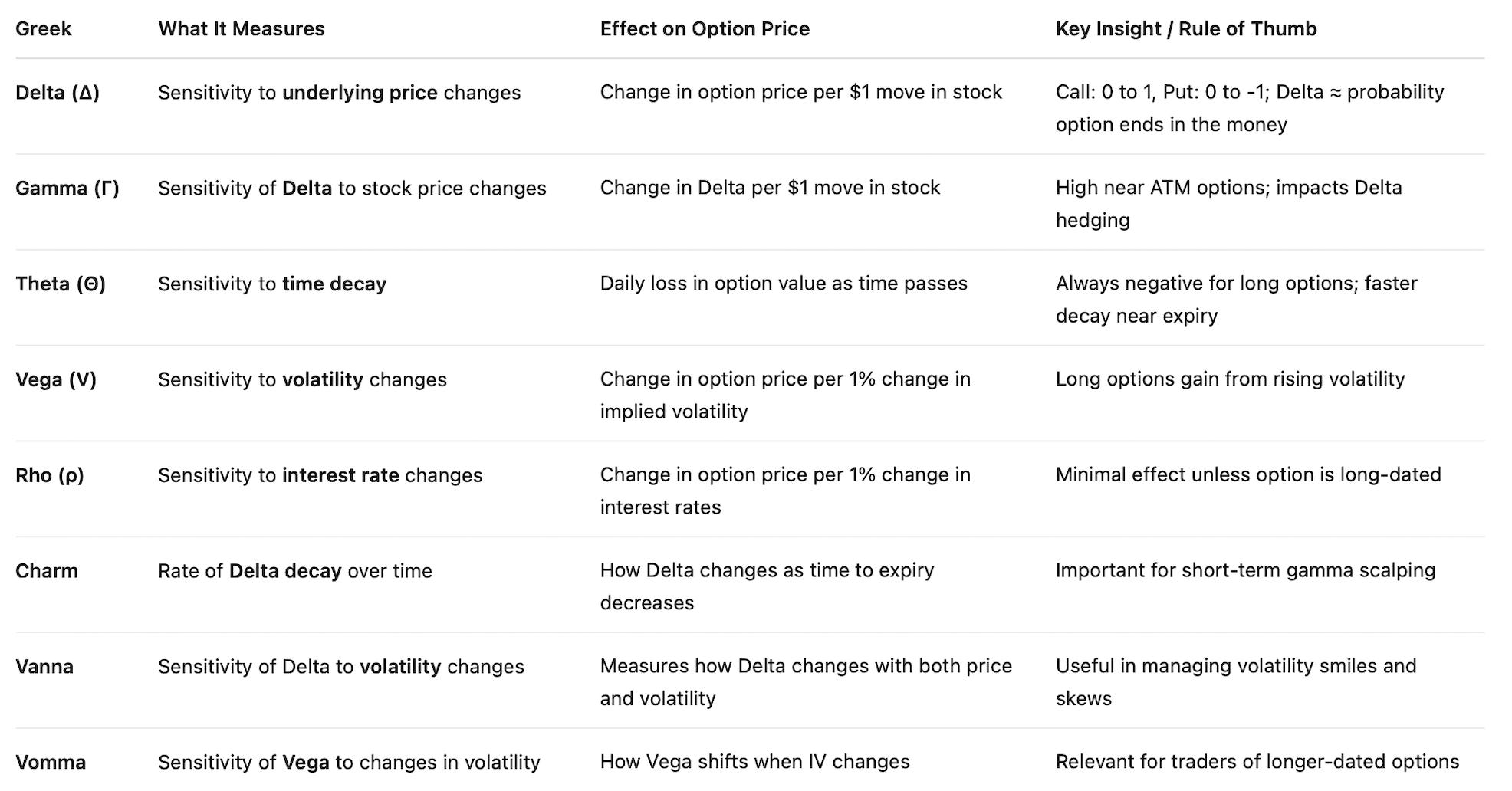

2. Delta: Choosing

How Bullish or Bearish We Want to Be

Delta defines directional exposure and probability.

For June 2026:

$15–$17 strikes: High delta (0.70–0.75)

$19–$20 strikes (ATM): Mid delta (0.58–0.62)

$22–$25 strikes: Lower delta (0.40–0.50)

Key principle in high IV:

Higher delta = more intrinsic value, less reliance on volatility staying elevated.

That’s why, when we’re bullish but cautious, we lean ITM or near-ATM, rather than chasing cheap OTM calls that require both direction and stable IV.

3. Vega: The Risk Most Traders Underestimate

At 82% IV, vega dominates the P&L.

Approximate impact:

ATM options lose ~$0.50 per contract for every 10-point IV drop

A move from 82% → 70% can erase gains even if price moves “your way”

Implications:

Long ATM/OTM options = vulnerable to IV compression

ITM options carry more delta per unit of vega

Vertical spreads naturally cap vega exposure

This is why we rarely buy naked options in high-IV environments without a strong volatility thesis.

4. Gamma: Why Long-Dated Trades Are More Predictable

With ~6 months to expiration:

Gamma is relatively flat across strikes

Small price moves won’t whip delta aggressively

Exposure evolves more slowly and predictably

That’s good for risk control—but it also means:

You need wider spreads to capture meaningful moves

Tight, short-term style strike spacing doesn’t work well here

5. Structure Selection: Why Spreads Beat Calendars Right Now

Bullish Call Spreads (Preferred)

Example logic:

Buy ~0.60 delta

Sell ~0.40 delta

Wide enough to matter (5–6 points)

Why this works here:

Delta-driven, not IV-dependent

Vega largely neutralized

Defined risk from day one

Minimal exposure to contango

This is boring, repeatable, and survivable—which is exactly what we want.

Calendar Spreads (Use With Caution)

Calendars struggle when:

Back-month IV is already expensive

Term structure is in contango

Volatility compresses or normalizes

In HL’s case:

You’re buying rich 6-month vol

Selling cheaper front-month vol

Exposed to a double hit if structure flattens

Calendars aren’t “bad”—they’re just structurally misaligned with this environment unless sized small or adjusted into diagonals.

6. Practical Risk Rules We Apply

A few non-negotiables in names like HL:

Assume slippage

Wide bid/ask spreads mean we plan for partial losses on entry/exit.

Size smaller than usual

High IV = faster P&L swings per dollar invested.

Spreads over singles

If we don’t have a volatility edge, we neutralize it.

Probability over payoff fantasies

Cheap options aren’t cheap if probability is low.

7. The Bigger Picture

This example isn’t about HL specifically.

It’s about process.

Every trade we put on follows the same logic:

Define volatility regime

Decide delta exposure intentionally

Control vega unless we want it

Use structure to express the view efficiently

Size for survival, not excitement

Markets decide outcomes.

We decide risk.

That’s the edge.

As always, more trade setups and live structures to follow.

~ Strategic Options Trader

Alternatively you may also consider the following - conditional premium selling :

• Your core position is a clean bullish vertical call spread

• This expresses the directional thesis

• Premium selling is added only when the market offers it.

You only sell short-dated calls after the market shows signs that time decay is likely to work in your favor, such as:

• A stall after a strong move (momentum pauses)

• A failed breakout (price can’t hold above resistance)

• A volatility spike (short-dated IV jumps relative to back-month IV)

At those moments, selling premium is opportunistic, not obligatory. You are reacting to conditions, not locked into defending a short option regardless of market behavior.

This approach solves the diagonal’s biggest weakness:

• You are never forced to cap upside during the strongest phase of the move

• You avoid the classic mistake of being directionally right but structurally wrong

• Premium selling becomes a tactical overlay, not a permanent constraint

In practice, this means:

• If the market trends cleanly → let the vertical work

• If the market chops or volatility spikes → sell calls then

• If momentum accelerates → stand aside and keep convexity

Think of it as: “Earn theta only when the market offers it — don’t sell theta just to finance the trade.”

So instead of: Diagonal first, manage later, you’re choosing:

• Vertical first

• Diagonal only when conditions clearly allow it

Great to hear, and very much appreciate your feedback on this. Let me know in due time how your approach has worked out ?